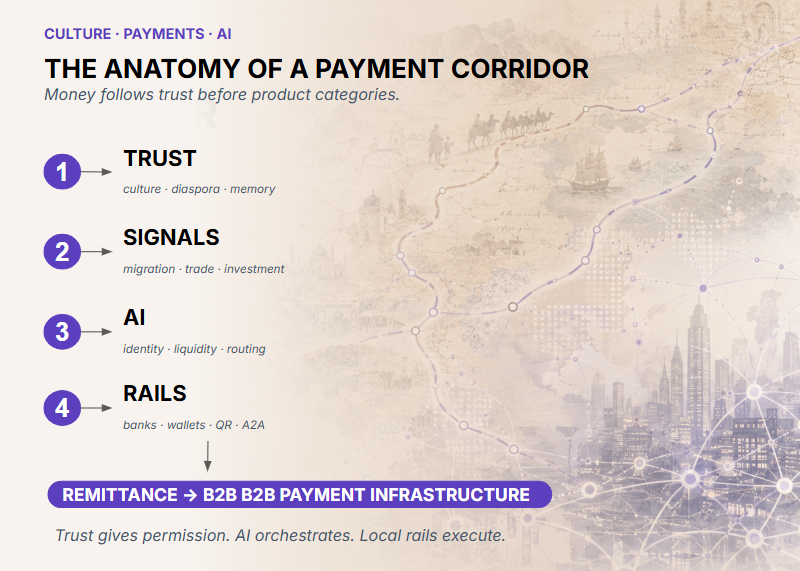

QR Payments In Europe

Europe has world-class payment rails but lacked an interoperable QR standard, leaving cross-border QR payments fragmented until the EPC’s MSCT QR (EPC024-22), Wero, PSD3 and a CEN standardisation push began harmonising things in 2026. Still, Europe is 5–10 years behind Asia and risks losing users or cross-border flows if standardisation moves too slowly.

Europe has instant payments. Europe has SEPA. Europe has some of the most sophisticated financial infrastructure on the planet.

And yet - until recently - a German tourist in Paris could not open a German banking app and scan a French merchant’s QR code.

Not because the tech was impossible. Because the QR codes were not interoperable.

Every provider had its own format. Every country had its own flavor. Every merchant had to juggle multiple codes like a payment-themed circus act. If complexity were a KPI, Europe was overperforming.

The European Payments Council has been trying to fix this since at least 2021.

Now, in 2026, things are finally moving.

The EPC’s MSCT QR standard - EPC024-22 - covers P2P, C2B, B2B, invoices, regular and instant SEPA transfers.

Wero - backed by 16 major banks including BNP Paribas - already counts 40 million enrolled users across Germany, France and Belgium, with QR built in natively.

PSD3 kicks in this year, pushing further harmonisation.

The standard is being submitted to CEN for formal European standardisation - the same body that sets industrial norms across the continent.

So yes, Europe is aligning. On paper, it is beautiful.

The honest summary? Europe is five to ten years behind Asia on QR adoption. Not because it lacks infrastructure. Not because it lacks capital. Because it lacked a shared standard. And in payments, without a shared standard, everyone builds a cathedral and no one connects the doors.

The irony is hard to miss.

While Europe was hosting conferences about ‘digital payment harmonisation’, Laos was putting four national QR schemes on one sticker. Ethiopia launched a national instant payment system in under a year. Belarus rolled out sovereign QR rails in months. No panel discussions required.

Europe’s advantage is scale, regulatory trust and deep banking rails. Its weakness is that consensus can move at the speed of a committee calendar.

The question is not whether Europe can standardise. It clearly can. The question is whether standardisation arrives before users get bored of waiting - or before non-European rails quietly capture cross-border flows.

At 8B, we watch both ends of this spectrum closely - markets moving fast because they have to, and markets moving slowly because they believe they have the luxury.

Sometimes that luxury expires.

You may be interested in: